Mortgage Update - December 30th, 2024

I can’t believe 2024 is almost in our rearview mirror. This week, I’m excited to share what Kreg and I expect from 2025 along with a 2024 year-in-review.

Happy New Year! We will see y’all in 2025 💪💪

We are posting regular content to Instagram (Nick | Kreg) and Facebook (Nick | Kreg) to help you and your buyers stay informed. Be sure to follow us!

Read time: ~4 minutes

Looking BACK on 2024 / Looking AHEAD on 2025

Here I am, a few days before the end of the year, and I find myself reminiscing about our bittersweet journey through 2024.

Kreg and I seldom discuss our successes, but in a market where transactions were up just 6% nationally, we managed to grow 13% in 2024! Our goal was to help 200 families finance homes this year and we ended up assisting 208 families.

We held our Rise & Thrive event to over 120 attendees in January, returned our focus to the basics, integrated more non-QM products into our business, started tracking key metrics a lot closer, made continued improvements on our best-in-class weekly newsletter and launched our monthly client-facing newsletter this year.

At the same time, we dealt with a very shaky housing market. Transactions near multi-decade lows, buyers priced out of the market, inflation rearing its ugly head again and mortgage rates stiff-arming us in the face and skyrocketing AFTER the Fed cuts rates.

We also witnessed friends in the industry hang up their real estate or mortgage license 😞. This industry is in a tough spot. Bittersweet is the only way to describe 2024.

But looking ahead to 2025, I do feel like we can be cautiously optimistic.

I think 2025 is going to look a lot like 2024, with some opportunities that may make it stronger 💪

Transaction volume will be flat, around that 4 million mark.

Average mortgage rates will range between 6.5% and 7.125%. Unfortunately we will start the year on the higher end of that range. We also won’t see rates that start with a “5” in 2025 unless there is some catastrophic black swan event.

I think new homes sales has peaked. Consumers are tapping out and cannot afford the higher purchase prices. It will be more expensive for builders to afford those lower advertised rates, which will 100% affect their profit margins in 2025. Until builders start producing smaller homes, I think they sell fewer homes next year.

2025 will be a buyer’s market. As I have discussed before, investors and cash buyers will do well next year.

A lot of people think first time homebuyers will struggle in 2025, but I wholeheartedly disagree. They have access to incredible financing options AND will be able to push sellers around a bit. Don’t ignore the first time buyers.

There are some tailwinds that may help the housing market in 2025. Months-of-supply is starting to increase nationwide, which may help bring prices lower. Sellers may need to increase offer stronger incentives to get their homes sold. Pent-up demand is ever-increasing. I am hearing more people talk about NEEDING to move vs. just wanting to move. Folks are tired of waiting for rates to pull back or prices to come down, and may start their search in 2025.

Those that are still in the industry have withstood some very low-volume years. If you’re still with us, you’ll make it. Just don’t give up.

Continuing Unemployment Claims Rise to 3-year High 🎢

Every Thursday, the US Department of Labor releases the weekly unemployment benefits report and the number of continuing claims is rising, briskly.

First time applicants landed at 219,000 which was just a hair shy of the forecasts.

However, continuing claims jumped by 46,000 to 1.91 million for the week of December 14th. That’s the most since the middle of November of 2021 when the country was still recovering from the pandemic.

Landing a new job may be harder and harder for those unemployed. Is demand for workers losing steam? If you’re paying attention, you’d hear more news about businesses closing up operations. Here in Central Ohio, Big Lots recently announced they were shuttering their entire fleet of stores nationwide, however, they did announce Friday they sold a small portion to Variety Wholesalers that will remain open. Party City, Container Store, CVS, Walgreens, TGI Fridays are all in trouble. At the end of Q3 2024, business bankruptcy filings in the US were up 33.5% annually.

This Friday, we won’t get the latest BLS jobs report like we usually do on the first Friday of the month. We’ll have to wait until January 10th to see if there is any trend developing in the US labor market, when the December 2024 data is released

Key Takeaway: The US labor force has seen modest unemployment application volume in recent weeks, but continuing claims have been on a pretty consistent upward trend. It appears job-seekers are struggling to quickly find employment, which may result in weaker consumer spending, slower economic growth and volatility.

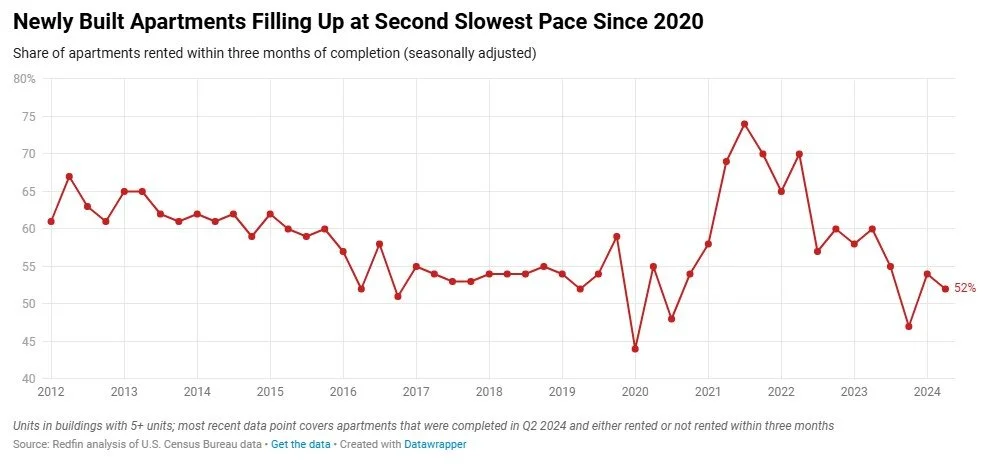

The Inflation Killer → Apartment Absorption Rate

Redfin recently reported on the speed at which newly built apartments are filling up…and it looks to be near historical lows.

The “absorption rate” is the percentage of new apartments rented out within 3 months of being finished. In Q2 2024, the rate came in at just 52%. The lowest on record was 44% in Q1 2020 vs. the highest on record at 74% in Q3 2021.

Supply is outpacing demand. A boom in new apartment construction spiked between 2020-202 when the US witnessed the highest level of apartment completions in 12 years.

Meanwhile, rental vacancy rates are the highest since Q1 2021 at 8%.

If apartment supply remains elevated for too long, we’ll see rental rates pull back. To juice demand, owners may need to offer concessions or even reduce rent to entice occupants, which could be a MASSIVE help to the inflation problem in the US.

As you all know (because you follow me and Kreg) shelter costs, which include things like rent and the cost of owning a home, are a big part of how we measure inflation. Everybody needs a place to live and it’s usually one of the biggest expenses for families. That’s why economists pay close attention to shelter costs as it makes up about 33% of the CPI measure.

Key Takeaway: More and more apartment complexes are coming online, which is causing a delay in filling up units with renters. Owners may need to juice demand by lowering rates, which would have an impact on shelter inflation. With shelter inflation making up about 33% of the measurement of inflation/CPI, we might see overall inflation pull back in a meaningful way giving some relief to the markets.