Mortgage Update - November 18th, 2024

Anybody else recovering from the Jake Paul/Mike Tyson match Friday night?

What a “fight” 🥱

Let’s dive into this week’s more exciting mortgage update 💪💪

We are posting regular content to Instagram (Nick | Kreg) and Facebook (Nick | Kreg) to help you and your buyers stay informed. Be sure to follow us!

Read time: ~4 minutes

CPI ⬆️ But Should Come Down ⬇️

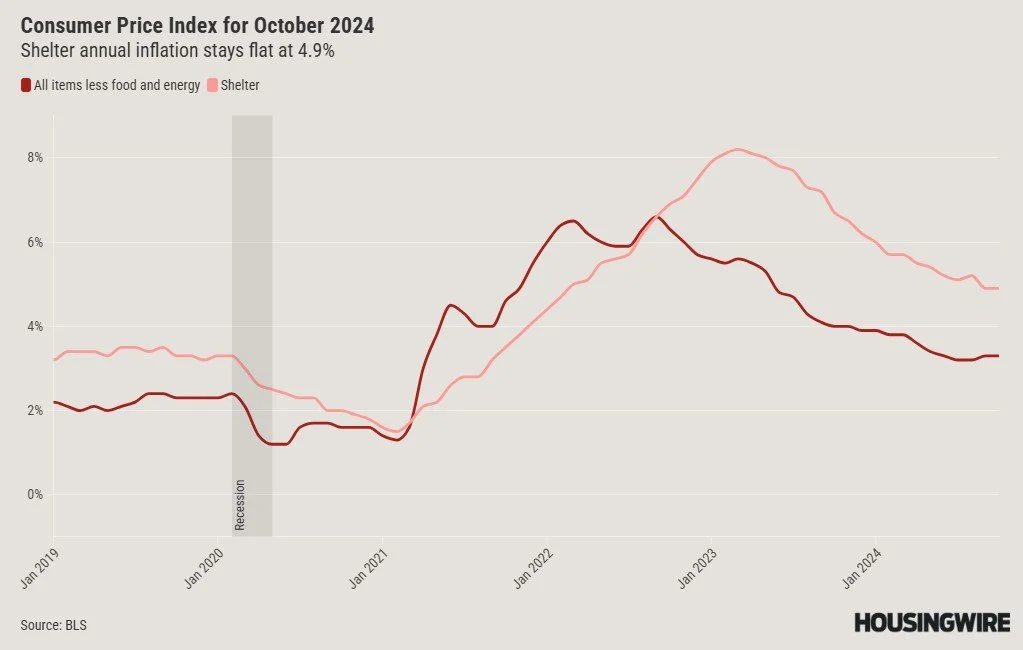

The anticipation of the CPI report Wednesday was about as big as the build up before the Jake Paul/Mike Tyson fight. And the results were about the same…a whole lot of nothing.

Headline inflation for October landed at 2.6%, up from 2.4% in September. Markets expected the slight increase. Core inflation (minus food & energy) was flat to September at 3.3%.

Shelter inflation rose (+0.4%), pulling CPI with it. While we are seeing house prices moderate a bit, shelter inflation calculations have a BIG lag as rents typically renew annually, not monthly.

While CPI ticked higher in October, it looks like the Fed should be able to wrestle inflation down to their 2% target in the first half of 2025.

Why?

It’s called the “base effect” and it’s the same reason markets didn’t flip out over the bump from 2.4% to 2.6%.

As you can see in the chart above, the Oct ‘24 number of 0.2% replaced Oct ‘23 of 0.1%. That replacement caused annual CPI to rise from 2.4% to 2.6% (rounding).

Take a look at the same chart during the January - April time period. In early 2025, we will drop some pretty large inflation numbers from the annual CPI calculation.

If we remain at the 0.2% level monthly, we should be on pace to hit 2.0% annually by April of 2025.

Key Takeaway: The Fed feels like their path to 2% inflation may play out by Spring of 2025. There are some potential headwinds like the uncertainties around the new Trump administration (spending, tax cuts, tariffs, immigration policy, etc.). If inflation can pull back to 2% and the job market experiences some turmoil, we might see incremental rate cuts from the Fed next year.

Buying a Home is Now a Luxury 💎

First time homebuyers make up smallest portion of purchases in at least 45 years.

The National Association of Realtors released some pretty jarring figures. Individuals buying a home for the first time make up just 24% of the market. That’s down from 32% last year.

Back in 2010, the first time buyers made up 50% of the market. We are currently half that! If you are looking for a sign of how sick the housing market currently is, this is it 🤢

Homebuyers are getting older. The average age has jumped DRAMATICALLY to 56 (up from 49 last year). First-timers are buying around 38 years old (35 last year).

First time buyers are faced with high home prices, high rates and limited inventory in most parts of the country making it a difficult/unhealthy environment for a large contingency of folks. These folks need to have the ability to buy a home to secure a foundation of financial independence in the long run.

Key Takeaway: We are seeing first time buyers priced out of the market. They have been near these lows before (1987). There are obvious signs of pent up demand. Once affordability is resolved, we should see a flood of buyers brought back into the market. This is a reminder to all buyers and agents, there are still great mortgage products out there for first time buyers. Don’t assume the average US interest rate is the same for everybody.

The American Dream is Now a Luxury 💎💎

$4,442,050 is now the cost of the American Dream 😭

I’m just going to leave this here for you to ponder.

Explain Open House Changes to a 5th Grader

On August 17, 2024, buyer-written agreements were required before touring a home with a real estate agent. But what happens if you're just popping into an open house?

Here’s something I created (based on NAR facts) to explain to my 9, 12, and 15-year-old daughters. If they understand it, your clients can understand it: