Mortgage Update - November 4th, 2024

Markets are still digesting the jobs report from Friday, the Fed announces their next potential rate cut on Thursday (moved from Wednesday) and we have a presidential election in there, too.

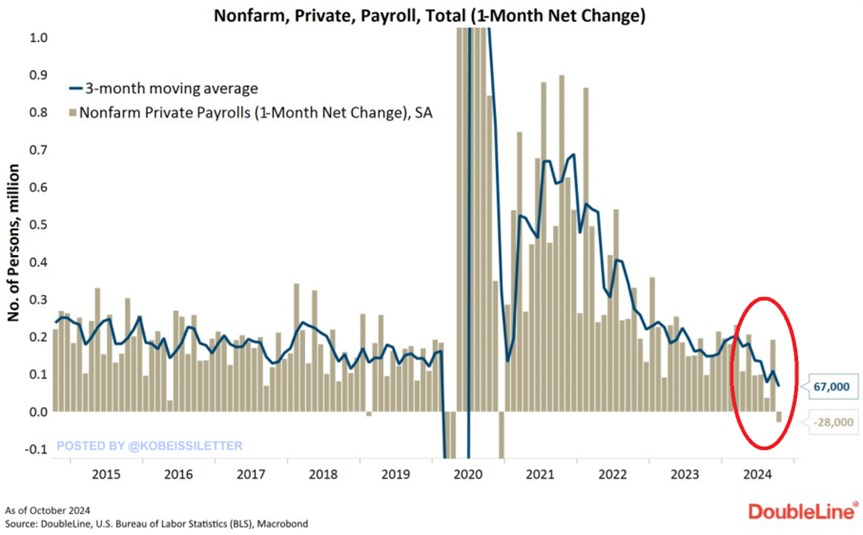

Huge Miss on October Jobs Report 🙀

The last jobs report leading into the presidential election dramatically missed expectations.

Nonfarm payrolls added 12,000 new jobs, which is down significantly from September and well below the 100,000 estimate.

Unemployment held at 4.1%.

Both hurricanes and the Boeing strike are being blamed for the shortfall.

Additionally, as we have come to expect, 112,000 jobs were revised OUT of the August and September reports.

If you remove the government jobs added in October, the economy actually LOST 28,000 jobs. These are referred to as nonfarm, private jobs.

You can see in the chart, a negative print on nonfarm, private payrolls isn’t very common.

This weaker report likely solidified at least a 25bps cut by the Fed at their next announcement this Thursday.

Mortgage rates remained relatively unchanged on Friday, likely due to the unemployment rate remaining flat. If that had reversed course and marched higher, I think we would have seen rates pull back a bit in anticipation of a stronger rate cut this week from the Fed.

“I’m NOT Buying a Home if insert name Wins!”

These last two weeks, I’ve fielded basically one question from agents.

Everybody apparently has a client watching the election and stating they will refuse to buy a home is the OTHER candidate wins the election.

I get it. This is a highly contentious, emotional election.

However, if your candidate loses, I promise it’s not the end of the world. We’ve all had our candidates lose in past presidential elections and the sun ALWAYS continued to rise.

Here’s what you tell those clients suggesting the economy will crash if their candidate doesn’t win : GOOD!

A weakening economy will pull interest rates down as the government tries to re-ignite investment.

Remember the Great Recession/Global Financial Crisis of 2007-2009? The Dot Com Bust? Or how about Covid 19?

The Federal Reserve pulled back rates aggressively during these periods of economic turmoil making money much cheaper to borrow.

Key Takeaway: Its education season in our industry. Buyers are nervous and scared. Its our job to guide them away from nervousness towards excitement without being insincere. Buying a home is a big deal, especially to first time buyers. Leverage the past to explain the present/future to set their mind at ease about the realities post election.

Appraisal Waiver Eligibility Expanded

Who wants more appraisal waivers?!

The Federal Housing Finance Agency (FHFA) announced several updates last week, but the most important is the expansion of appraisal waivers for properties up to 90% loan-to-value (LTV), up from 80% LTV currently.

They are even allowing inspection-based appraisal waivers up to 97% LTV, though many lenders don’t allow inspection-based reviews.

Why does this matter?

Reduced Closing Costs : In an already unaffordable environment, this helps buyers save $500-$750 at closing.

Reduced Underwriting Timeline : Lenders can close loans faster if they aren’t waiting for appraisals and remedies.

Stronger Pre-approval Letters : Ask any listing agent, they perk up when they see an appraisal waiver noted on a pre-approval letter.

The update should go into effect in early 2025 for Conventional financing only. Once it drops, lenders can run properties through the automated underwriting system to check waivers on loans with as little as 10% down.